Chairman Rabbit on U.S. administration's tariff retreat regarding Chinese electronics

"For China and the rest of the world, the task is clear: see through America’s logic, abandon illusions, and focus on our own path."

A week ago, after U.S. President Donald Trump threatened to impose an additional 50 percent tariff on China in response to Beijing’s proposed countermeasures, two prominent Chinese internet commentators -- Ren Yi (better known by his online alias "Chairman Rabbit" or 兔主席"Tù Zhǔxí" in Chinese) and Liu Hong, who writes under the pen name "Niu Tan Qin" (牛弹琴) -- published similar analyses on their WeChat blogs, revealing that China had prepared six specific countermeasures to address Trump’s tariff escalation, which are:

1. Suspend cooperation on fentanyl

2. Further restrict U.S. exports of soybeans, sorghum, and other products to China

3. Restrict U.S. poultry exports to China

4. Impose countermeasures in the services trade

5. Reduce or ban U.S. film exports to China

6. Investigate U.S. companies’ intellectual property (IP) gains in China

(Zichen Wang covered Chairman Rabbit’s piece on Pekingnology, while Fred Gao shared Liu’s analysis on Inside China.)

So far, at least one of the six measures has been implemented -- China on Thursday announced the plan to moderately reduce the number of U.S. films imported, according to Xinhua News Agency:

A spokesperson for the China Film Administration said that the adjustment follows market principles and reflects audience preferences, as the United States' recent hikes in tariffs on Chinese imports are bound to impact Chinese audiences' interest in U.S. movies.

As the second-largest film market in the world, China has always pursued a high level of opening-up, and will introduce more excellent films from other countries to meet market demand, said the spokesperson.

On Sunday, Chairman Rabbit posted a follow-up analysis on Trump administration’s tariff retreat regarding Chinese electronics—the Chinese version on his WeChat blog and the English version on his X (Twitter) account.

With his permission, I’ve republished his piece in today’s newsletter.

On Saturday, the U.S. government suddenly announced the exemption of 20 categories of electronic and tech products—including semiconductors, computers, tablets, and Apple Watches—from "reciprocal tariffs." These goods, largely imported from China (amounting to roughly $100 billion annually), account for about a quarter of China’s total annual exports to the U.S. This move effectively excludes a significant portion (and the highest-value portion) of tariffs on Chinese goods. Recently, China and the U.S. have been engaged in an intense trade war, and Trump’s policy reversal amounts to a public slap in his own face, putting himself in a politically vulnerable position and limiting the White House’s future policy options.

Given the frequent and chaotic shifts in the Trump administration’s tariff policies recently, it’s useful to take a moment to sort through the timeline.

(or skip to Part II: Analysis and Commentary)

Part I. A Recap of Trump administration’s Trade War (and Tariff Policies Targeting China):

In late February, the Trump administration first imposed a 20% "punitive" tariff on China, citing "fentanyl" as the reason.

On April 2, the Trump administration announced a new round of tariffs set to take effect on April 9, including:

A 10% universal tariff on all countries and regions.

"Reciprocal tariffs" on about 60 countries and regions, with varying rates. China’s rate was set at 34%.

China retaliated (also imposing 34%), prompting Trump to escalate further, leading to a spiral of tit-for-tat measures.

The final outcome was a 125% "reciprocal tariff" imposed by the U.S. on China, on top of the earlier 20% fentanyl tariff—totaling 145%. China retaliated with a 125% tariff.

(Note: This does not include the roughly 20% weighted average tariffs imposed during Trump’s first term, which the Biden administration largely retained.)

During this period, the U.S. experienced a simultaneous stock and bond market downturn. On April 9, Trump announced a 90-day suspension of "reciprocal tariffs" on other countries and regions while keeping the 10% universal tariff—and maintaining all tariffs on China, singling it out as the primary target.

On April 12, Trump announced an exemption for all electronic products from "reciprocal tariffs"—meaning Chinese electronics would still face the 20% base tariff but not the additional 125% "reciprocal tariff."

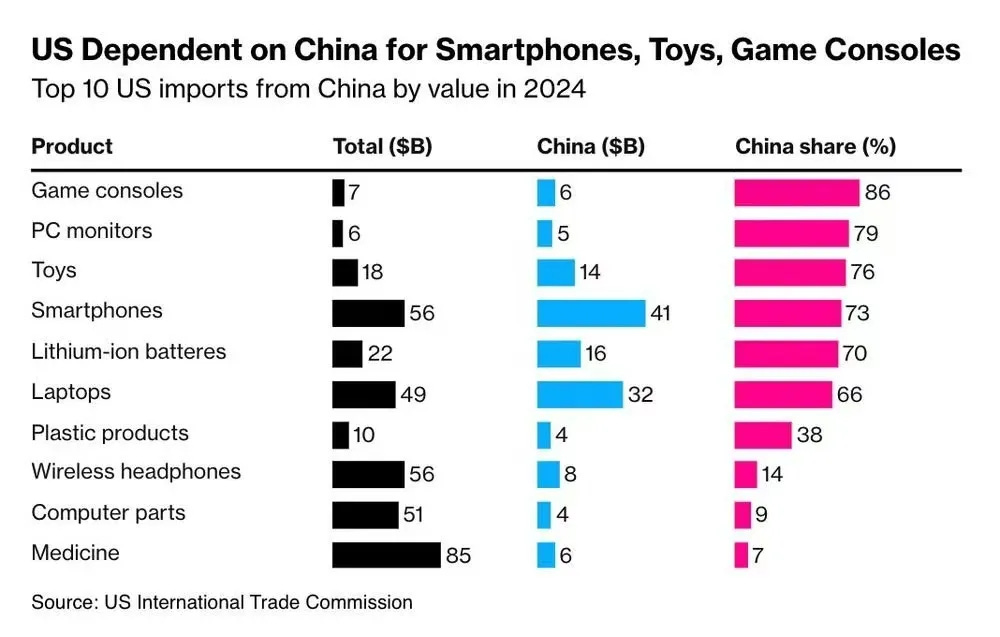

According to U.S. data, the exempted tech products account for about $100 billion of U.S. imports from China in 2024, or roughly 23% of total imports from China. Among these, smartphones and computer monitors are particularly dependent on Chinese imports, with shares as high as 81% and 78%, respectively. (See the data chart below for details.) The U.S. remains highly reliant on China for electronics, with no short-term alternatives available.

Every policy announcement by Trump has been highly provisional. For example, when announcing the suspension of "reciprocal tariffs," Trade Representative Jamie Greer was still explaining the tariff logic to bipartisan lawmakers in Congress—completely caught off guard. Before the weekend exemption for electronics/tech products was announced, senior cabinet members were still aggressively promoting the tariff policy’s "reshoring" narrative. Commerce Secretary Lutnick, in a CBS News interview just last Sunday, claimed: "great American workers" would soon be employed in new factories built and operated in the U.S., declaring, " army of millions and millions of human beings screwing in little screws to make iPhones, that kind of thing, is going to come to America" As recently as Saturday, White House Press Secretary Karoline Leavitt said: "The President has made it clear—America cannot rely on China to manufacture critical technologies such as semiconductors, chips, smartphones, and laptops", and "Companies are hustling to onshore their manufacturing in the United States as soon as possible. "The policy reversal is a resounding self-inflicted slap in the face. And make no mistake—the whole world is watching and listening: That loud slap? You delivered it to yourselves.

These policy reversals have been abrupt and theatrical, leaving not just the outside world struggling to keep up—even Trump’s own team can’t stay synchronized. On one hand, they must continue toeing the line, lavishing praise on Trump ("Trump is always right," "a masterclass in the art of the deal"). On the other, they’re forced to publicly defend the indefensible, spinning defeats as victories and praising the "emperor’s new clothes." Meanwhile, behind the scenes, they’re scrambling to clean up the mess. It’s a chaotic, humiliating tightrope act.

Trump’s exemption for electronics marks a critical collapse in his trade war against China. To borrow his own words against himself: "you don’t have the cards". He can keep performing the "emperor’s new clothes" routine, declaring "historic wins," but the market sees right through it. His team can only curse privately while groveling publicly, desperately brainstorming: How do they salvage their own reputations within this clown show? How do they minimize the damage while still keeping Trump—their unhinged boss—happy?

And if you doubted whether this Trump administration truly is a clown show, they’re doing everything possible to prove it.

Below is some further analysis and commentary.

Part II. Analysis and Commentary

The First Retreat on "Reciprocal Tariffs": Trump administration’s Concession to Wall Street: On April 9, Trump suspended "reciprocal tariffs" on other countries and regions because the U.S. market was experiencing a simultaneous stock and bond sell-off—particularly when investors began dumping U.S. Treasuries, driving yields up sharply. Frightened, Trump had no choice but to back down. That retreat was a concession to the bond market, capital markets, and Wall Street.

This Retreat on Chinese Electronics: Trump administration’s Concession to Main Street: This time, Trump’s exemption for Chinese electronics is a concession to ordinary Americans—since the U.S. remains highly dependent on China for these products, with no short-term alternatives. Imposing tariffs would only pass costs onto U.S. consumers, fueling inflation and creating a political disaster for Trump and the GOP. Remember, Trump campaigned on "taming inflation." Yet since taking office, he has done nothing to lower prices, instead relentlessly hiking tariffs, which has only worsened inflation expectations and pushed the U.S. toward stagflation.

A Boon for Big Tech and Big Corporate: Apple and other tech firms as well as retailers are the direct beneficiaries of this exemption. They can breathe a sigh of relief: They can continue manufacturing electronics in China for now, without immediately needing to restructure supply chains (assuming restructuring is even feasible). But as long as companies hold off on reshoring investments, the U.S. won’t regain these industries.

China’s "Two Models". Looking at the industries, if we crudely categorize China’s major exports to the U.S. by their position in the value chain, we see two broad types:

1)Yiwu Model: Lower-value-added goods like toys, plastic products, apparel, and furniture.

2)Big Tech Model: Higher-value-added electronics/tech products—from Apple, HP, Microsoft, Samsung, Sony to Hisense, TCL, Lenovo, and Foxconn, spanning both B2B and B2C sectors, including both branded and contract manufacturers. These goods involve complex processes and higher margins. (Of course, this is an oversimplification—Yiwu also produces some high-value goods, and mid-sized firms make electronics. Reality is a spectrum where products occupy varying positions along the value chain.)

What Trump administration Really Wants: High-End Manufacturing (Where Tariffs Might Help):

Trump’s original vision for tariffs included some long-term thinking—reshoring manufacturing to ensure supply chain security and create high-quality jobs. But industries and products differ. Today‘s U.S. lacks the capability, conditions, or will to bring back low-value-added sectors like toys, apparel, or plastics. Notice how Trump officials, when promoting reshoring, only ever mention high-value industries like autos, semiconductors, and electronics—never toys or clothing (which makes their tariffs on these goods utterly devoid of industrial logic).

Most would agree that tariffs, while not sufficient alone, may be a “necessary” condition for reshoring. Without steep tariffs on electronics, those industries won’t return. But even with tariffs, success is far from guaranteed.

What Kind of Tariffs Would Actually Support U.S. Industry?

This leads to the most critical point: From an industrial logic perspective, if the U.S. government wants to use tariffs to steer (or force) corporate behavior, those tariffs must be *long-term and predictable*. The necessary conditions are as follows:

Targeted, not blanket: Tariffs should support specific industries as part of a deliberate industrial policy, not indiscriminately applied to all countries, regions, or products.

Universal, but not country/jurisdiction-specific: To reshore industries, tariffs must apply equally to ALL trading partners. If only one jurisdiction (e.g., Mainland China) is targeted long-term, supply chains will simply shift elsewhere—not return to the U.S.

Permanent, not temporary: Sector-wide tariffs must be established as long-term national policy, integrated into a broader industrial strategy.

Bipartisan consensus: There must be clear, durable, and public agreement across parties and institutions, ensuring tariffs outlast any single administration.

Legislative, not executive: Tariffs should be codified by Congress, not implemented via executive order (which can be reversed, challenged in court, or scrapped by the next president).

Time horizon aligned with investment cycles: Factories and supply chains take years—easily beyond a 4-year presidential term—to build. For tariffs to work, firms must trust they’ll remain for 10–15 years with near certainty. Only then will they act.

Tariffs alone are insufficient: They’re necessary but not sufficient condition. Complementary policies—regulatory reforms, workforce training, infrastructure, and anti-addiction measures (U.S. manufacturers complain they can’t find workers sober from 9 AM to 5 PM due to rampant substance abuse or lack of work ethics)—are critical.

Shared Sacrifice: Reshoring inflicts short-term pain: scarcity, inflation, lower living standards, corporate losses, market volatility. Society must unite behind a "weather the storm" mentality to endure transition. If every market dip triggers panic, lobbying, partisan fighting, and policy reversals, long-term industrial revival is impossible.

The Verdict: America’s political system—its polarization, policy whiplash, and institutional design—proves it lacks the foundation for long-term industrial policy. Its governance was not designed and built for this.

The Inevitable Outcome of Policy Volatility and Short-Termism: Corporate Wait-and-See

If there were ever a leader least suited to implementing long-term policies, it would be Trump. If there were ever an administration least capable of executing a long-term industrial strategy, it would be Trump’s. Today, U.S. tariff policy flip-flops erratically—imposed one day, suspended the next; raised abruptly, then slashed; universally applied, then selectively exempted; declared "permanent," only to become "negotiable." The objectives, strategy, tactics, and messaging are utterly incoherent, offering no predictability or certainty to businesses.

For companies, the dumbest move would be to hastily comply with Trump’s whims—say, relocating supply chains from Country A to Country B—only for the U.S. to suddenly strike a trade deal with Country A, dropping tariffs, or to impose new tariffs on Country B after it becomes the latest trade deficit villain. Such whiplash could render their supply chain investments worthless overnight.

Under these conditions, no rational firm will commit to major decisions. Instead, they’ll wait and watch. Building a factory takes 4–5 years; the safest bet is to endure the remaining 3.5 years of Trump’s term and see if the primary source of uncertainty—Trump himself—can be removed. But this corporate paralysis also suppresses investment, further denting the economy.

Projecting the Industrial Outcomes of Trump administration’s Tariffs

Now let’s assess the likely results of Trump’s tariff policies:

Low-value industries Yiwu Mode—"External Cycle"

For sectors like toys, plastics, apparel, and footwear, reshoring to the U.S. is impossible unless America imposes PERMANENT high tariffs—and absorbs massive short-to-medium-term economic pain. Otherwise, outsourcing firms will merely optimize around country-specific tariffs (e.g., China), shifting supply chains between foreign nations rather than returning to the U.S. The outcome would be, whatever country inherits production will see its trade surplus with the U.S. surge (as happened with Vietnam and Mexico post-2018), but America’s TOTAL trade deficit will remain largely the same.

At this point, Trump’s tariffs have lose all its economic rationale, retaining only a political one: "de-risking" by reducing reliance on any single country. But this is self-defeating—if security is the goal, shouldn’t the focus be on high-value tech, instead of T-shirts? Meanwhile, the best lesson that every nation (including China) has learnt by now is to prioritize reducing dependence on the U.S. market.

High-value industries—Status quo dependence on China

Given China’s dominance in electronics/tech, Trump—constrained by economic and political realities—has already exempted these products from "reciprocal tariffs." Most supply chains will stay in China, dashing any reshoring hopes.

This failure isn’t just economic; it’s strategic. If tariffs were truly about "security," why spare iPhones and semiconductors while hammering sneakers? The contradiction exposes the policy as hollow theatrics.

Bottom line: Trump’s tariffs are NOT going to revive U.S. manufacturing. They’ll just shuffle deck chairs on the global trade Titanic—while convincing the world to build lifeboats away from America.

The Real Damage of Trump administration’s Tariff Policies

As the above analysis shows, Trump’s tariffs fail to address any problem—whether judged by economic/industrial logic or political rationale. Instead, they create massive new ones. Rolled out recklessly and then reversed 180° under pressure, these policies have turned into a farce. Trade wars have no winners, and while we need not frame this as a zero-sum "U.S. loses, China wins" dynamic, the undeniable reality is that the Trump administration (and by extension, the U.S. government) emerges as the biggest loser: It has shattered market confidence, demolished trust in its governance competence, strained alliances, and forced businesses and consumers to bear the costs. This represents a comprehensive U.S. defeat—politically, economically, institutionally, and ideologically. The only valid lesson here is that all nations (including U.S. allies) must systematically reduce dependence on America—whether in security, technology, or trade.

After Repeated Defeats, Trump administration Has No Path to Recovery

It’s critical to recognize that Trump and his team DID harbor a long-term instinct to reshore industries through tariffs. But policymaking isn’t a game—it’s a complex interplay with markets, industries, political forces, and the public. Flip-flopping equals political suicide. Since March, Trump has U-turned on multiple tariff policies, retreating each time under market and media backlash. Battle after battle, he has lost.

Now, no one believes he’ll really reinstate "reciprocal tariffs" after 90 days, because U.S. Treasuries would crash again, cornering him in the exact same position. The same dynamic will replay for tariffs on China and others: Businesses, markets, politicians, and the press will force another retreat. Through “repeated games”, the market has learnt to exploit Trump’s weaknesses and confirmed that resistance works.

With each prior defeat, Trump’s chances of a comeback dwindle further. He has already overdrawn his political capital and exposed his vulnerabilities—irreversibly.

11. Three further takeaways:

For businesses, the safest approach is to stay put—wait and watch. Trump has less than 4 years left (from now till effectively election in Nov 2028) , which will pass in a blink. The best strategy is to maintain flexibility and adapt as needed.

The riskiest move is to make hasty investment decisions based solely on Trump’s rhetoric, which could leave companies exposed. Instead, firms should base long-term strategic choices on broader U.S. socioeconomic and political trends—focusing on potential bipartisan consensus rather than Trump’s unpredictable actions.

The smartest play is to "buy the dip."** Whenever Trump rolls out an aggressive policy and markets teeter near collapse, that’s the time to invest—because history shows he’ll likely back down under pressure and declare victory. Take his social media posts literally when he says, "Now is the time to buy." He and his inner circle may well have already positioned themselves accordingly.

12. America's Real Problem: Domestic Inequality.

The root issue in the U.S. is domestic wealth disparity, with its core contradiction being internal class conflict. Its actions are merely an attempt to externalize these domestic tensions.

As a nation and as an economy, the U.S. has benefited immensely from globalization. One critical figure highlights this: the sales revenue of U.S. companies in China—largely generated by American firms manufacturing goods or providing services locally. In 2022, U.S. corporate sales in China reached US$490.52bn(~500bn). In 2024, China’s exports to the U.S. totaled 524.66bn(also ~500 billion), a significant portion of which consisted of products made in China by U.S. companies and shipped back home.

Who reaps the lion’s share? U.S. multinational corporations and financial capital.

America as a whole has gained from globalization—but all the benefits have been captured by its corporations and capital elites. By offshoring production, capitalists abandoned American workers, leaving them with little to show for globalization’s gains. At its core, this is a “class struggle” between U.S. capitalists and workers—a domestic issue of economic distribution, unrelated to third-party nations.

Any one who is familiar with theories of left-wing political economy would understand: when imperialist nations fail to resolve internal class contradictions, they export their conflicts abroad. A century ago, this meant war and colonization; today, it takes the form of trade wars. The tactics change, but the essence remains.

We can take this analysis further: The American bourgeoisie’s strategy is to redirect domestic class conflict into nationalistic tensions between the U.S. and other countries, scapegoating external actors for their own political failures.

13. Only Socialism Can Save America

Thus, what America needs is not to disrupt global trade but to make the right political choice: reforming its domestic wealth distribution system. In fact, addressing inequality through political means may be easier than rebuilding industries.

Why? Because redistribution is primarily a political decision, whereas reviving manufacturing requires aligning policies, infrastructure, labor markets, and corporate participation. Moreover, in the age of technological revolution, industrial revival ≠ job creation. Even with perfect policy, America’s next industrial wave would be automation and AI-driven, generating few jobs. "Offshoring" would simply become "robot-outsourcing," deepening class strife between unemployed workers and tech-reliant corporations.

So, the conclusion remains: Only Socialism Can Save America. By “Socialism” we mean social democracy or democratic socialism. The label does not matter, the essence does.

Yet this solution is politically unattainable—because the American society still largely rejects socialism.

Result? The U.S. will not be able to resolve its domestic problems, and will keep externalizing the conflicts and destabilizing the world—especially China.

For China and the rest of the world, the task is clear: see through America’s logic, abandon illusions, and focus on our own path.

Very painful to read as an American. I have to agree with the analysis, however, the imbalance of trade needed to be elevated and now needs to be addressed in a rational way. The means do not justify the outcome.