How can China overcome challenges to realize a 5% annual economic growth? | GRR x Baiguan

Analysis from former governor of China's central bank and notes by Baiguan

Today, we present a collaborative piece between Ginger River Review (GRR) and Baiguan, delving into an article on China's economy which was published on Sept. 19 on the official newspaper of the Chinese People's Political Consultative Conference (CPPCC), China's national political advisory body.

This article comes from a speech by Yi Gang, deputy head of the CPPCC's economic committee and ex-governor of China's central bank. Originally titled "当前经济运行中的几个特点" (Several characteristics of the current economic operation), the article is translated by GRR and enriched with notes and data from Baiguan. Their insights bring a fresh, verified perspective on Yi Gang's observations.

Several characteristics of the current economic operation 当前经济运行中的几个特点

Currently, China’s economy is still in the recovery phase following the impact of the pandemic. We must have confidence and patience.

As the balance sheets of economic entities continue to be repaired, residents will gradually increase consumer spending, thereby generating income and more consumption. Internationally, it takes about a year for consumption to fully recover from the pandemic, and our country is only half a year in, so recovery still requires time. However, it's also worth noting that the economic recovery has slowed since the second quarter, with the manufacturing PMI shrinking for three consecutive months, indicating weakened economic momentum and market confidence.

I suggest that China moderately strengthen macroeconomic policy adjustments to effectively support the expansion of domestic demand and promote a positive economic cycle, jointly pushing to achieve this year's expected growth target of around 5 percent.

The current economic operation has several characteristics:

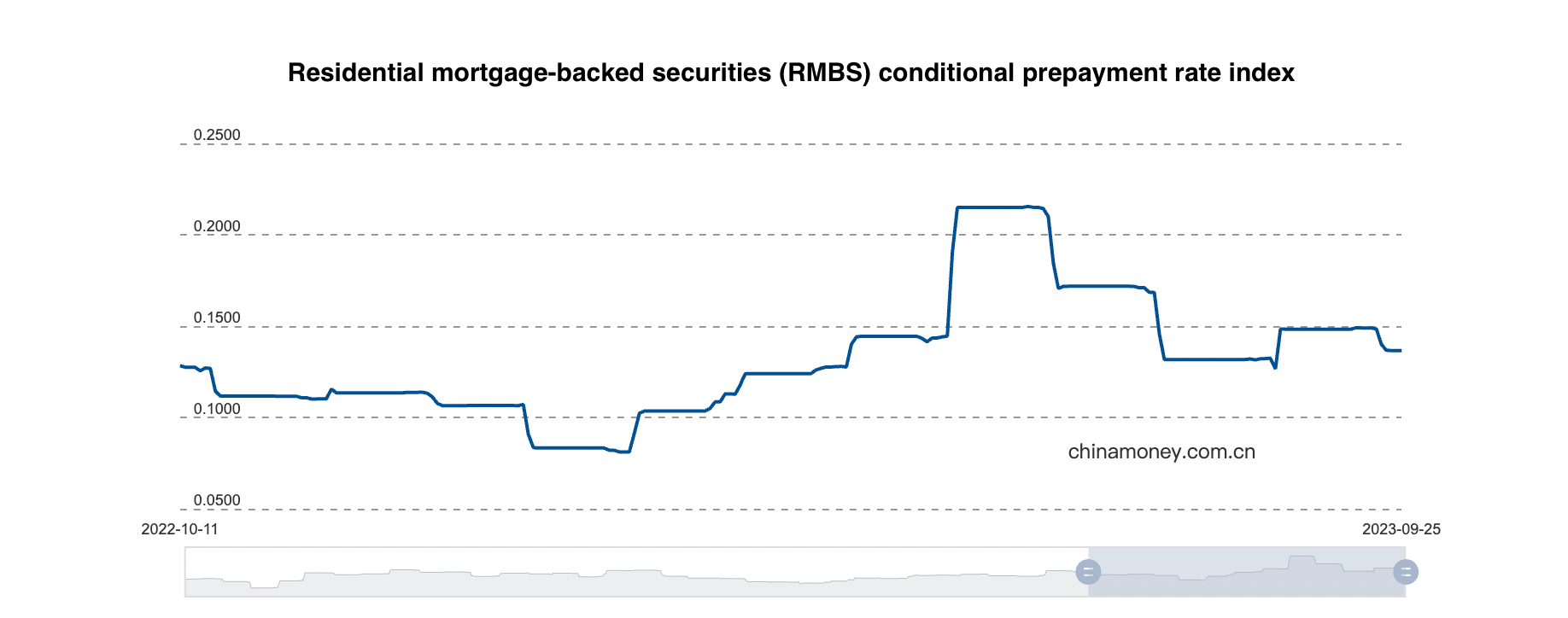

The household sector is spending less and repaying loans in advance. In April and May, the retail sales of consumer goods grew by an average of 2.6 percent and 2.5 percent respectively over two years, far below the pre-pandemic level of around 8 percent. Households have expectations of wage cuts and are cautious, preferring to increase savings and reduce debt. In the first five months, the proportion of new fixed deposits to new M2 reached 90 percent, 13 percentage points higher than the same period last year. The phenomenon of early repayment of individual housing loans has increased, and some micro-entities may lean towards "minimizing debt".

Note: Recently, China has introduced a series of stimulus measures such as "recognizing property, not loans", lowering down payments, and reducing interest rates. The scale of this interest rate adjustment for existing home loans is substantial, potentially saving residents a significant amount of interest. We have observed that the early repayment rate for residential mortgage-backed securities (RMBS) has decreased recently, indicating a trend of reduced early loan repayment.

On the household consumption side, we have observed continued signs of recovery, especially in the luxury & non-essential categories. Across Tmall, JD and Douyin, categories like Bags & Accessories and Jewelry & Gifts show strong Gross merchandise value (GMV) growth, especially in Q2. Digital Electronics also saw a jump in GMV and average selling price (ASP) in July and August 2023. This suggests that consumer confidence is improving as discretionary spending increases.

However, other categories such as car accessories, clothing, computer & office, general household items, and home appliances have experienced consecutive declines in average selling price (ASP). This suggests that consumers are seeking more affordable options, indicating a degree of caution in their spending.

Across major online recruitment platforms in China, we have observed a slow and stagnant improvement in the average salary since 2023. This lack of growth in income expectations may further contribute to caution among households.

Differentiation in the corporate sector is severe. This year, new credit has mainly flowed to state-owned sectors and the innovative technology domain. Investment in the new energy sector is growing rapidly but is of limited scale, and the real estate sector's contribution to the economy is insufficient. In the first five months, private investment decreased by 0.1 percent year-on-year. The confidence of private and small-medium enterprises, which contribute significantly to GDP and employment, needs boosting.

Note: On major Chinese online recruitment platforms, we've noticed a slow uptick in job postings since the start of 2023. Notably, private enterprises are recovering more slowly than state-owned companies. However, they're outpacing public firms, foreign entities, and Sino-foreign joint ventures, demonstrating their resilience.

The risk of local government debt has increased. Due to the impacts of the pandemic and adjustments in real estate, conflicts between local fiscal revenue and expenditure have become more prominent. Bonds issued by local government financing vehicles (LGFV) are at the repayment peak, and the link" from local governments pulling in money from land sales to infrastructure investment" is hard to maintain. With low project returns and fragile repayment ability, local governments' capacity to perform is constrained.

Risks in the real estate market have not been fully addressed. After the brief recovery in the first quarter, the real estate industry is again on a downward trend. In the first five months, real estate development investment decreased by 7.2 percent year-on-year, and the sales area of newly-built commercial housing decreased by 0.9 percent. The financing capabilities of real estate companies remain weak, and liquidity issues have intensified. In the long term, affected by factors such as the slowdown in urbanization and the population aging, the overall demand for home purchases may fall to a new level.

Note: According to data from Baiguan (as of September 17), in the week following the introduction of the new "recognizing property, not loans" policy in first-tier cities, there was a continued increase in the number of property viewings and transactions of the existing homes. This suggests that policy measures are bolstering a steady recovery in the real estate market.

The external sector has entered an unstable situation and may compound with insufficient domestic demand. U.S. interest rates might remain high for a while, its economic and financial risks are rising, and the global economy is slowing down. The weakening external demand poses significant challenges to China’s trade stability.

There's no basis for deflation in the trend of prices, but supply-demand balance issues should be noted. Deflation often accompanies demand contraction. However, China’s domestic demand is still recovering, and monetary and credit growth is rapid, not matching typical characteristics of deflation. In June, the year-on-year CPI remained stable, and the PPI decreased by 5.4 percent. As the base figure drops and intrinsic economic momentum strengthens, the CPI core is expected to rise moderately, and the PPI is predicted to rebound in the fourth quarter.

Employment is generally stable, but structural contradictions are significant. As artificial intelligence gradually replaces intellectual labor jobs, structural mismatches in labor supply and demand might persist long term.

Note: As of July 2023, there has been a marked increase in job demand related to AIGC/GPT, predominantly in sectors like information technology, manufacturing, and scientific research. Current job postings suggest that hiring is in its initial phase and might not significantly impact the broader workforce in the short term. However, this trend could drive structural shifts over the long run. Leading the charge are internet giants like Alibaba, Baidu, and Byte Dance. In the manufacturing realm, automakers like Geely and Li Auto are also ramping up AIGC-related hires, focusing on innovations in intelligent cockpits and human-vehicle interactions.

Monetary policy has strengthened counter-cyclical adjustments to help stabilize the broader economy. In the first half of this year, financial institutions added 15.7 trillion yuan in new RMB loans, a year-on-year increase of 2 trillion yuan. Financing costs have been stable and decreasing, with the average corporate loan interest rate at 3.96 percent in the first five months, down 0.39 percentage points year-on-year. In June, the guiding rate for monetary policy operations was further reduced by 10 basis points, driving the loan market rate down simultaneously.

Due to factors such as the US dollar maintaining a strong position and the domestic concentrated foreign exchange purchases during the summer, the RMB exchange rate has weakened, but it has recently rebounded.

In response to the above characteristics and existing issues, here is my advice:

We should leverage the role of structural monetary policies, tailoring strategies to different cities to support both essential housing needs and housing quality improvements. The low rent-to-sale ratio is a significant factor restricting the sustainable operation of affordable housing. For break-even in finance, the rent-to-sale ratio of affordable housing generally reaches 3 percent - 4 percent. Still, the current level is about 1 percent -1.5 percent. In response, the People's Bank of China has introduced a rental housing loan support plan, providing low-cost funds with a benefit of more than 1 percent. With appropriate local government financial subsidies, this plan promotes local governments' acquisition of existing homes and expands the supply of affordable rental housing, with pilot programs already in eight cities.

We should push urbanization through reforms of China's system on residence permits, or "hukou”, to unleash consumption potential. Scholars have estimated that through household registration reform, the consumption willingness of migrant workers and new urban residents can be increased by 23 percent. Therefore, better guarantees in housing, medical care, children's education, and social security should be provided to migrant workers working in cities. At the same time, it's essential to maintain a certain degree of labor mobility between urban and rural areas, different cities, and the eastern and western parts, acting as an inherent stabilizer for the Chinese economy.

We should establish an electricity pricing system during peak periods in summer executed by provincial governments, raising electricity prices during peak usage periods. China leads the world in electricity consumption, reaching 8.6 trillion kWh in 2022, more than twice the U.S. (4.1 trillion kWh). Per capita electricity consumption is about 6100 kWh/year, nearly double the global average (3200 kWh/year). Yet, China's electricity prices are relatively low on a global scale, leading to domestic power wastage. Some regions' nighttime lighting in China is brighter than major metropolitan areas in Europe and the U.S. Pricing mechanisms are one of the more effective policy tools. Consideration should be given to appropriately raising peak electricity prices in summer, alleviating electricity rationing pressures. Simultaneously, we can promote carbon emission reduction from the demand side to help achieve carbon peak and neutrality goals. Enditem

*About Baiguan.news: A newsletter crafted for anyone with a real stake in China. Powered by extensive on-ground data, seasoned cross-border experts, and advanced technology, Baiguan delivers credible, multifaceted, and actionable insights. Think of Baiguan as your reliable, no-nonsense ally for doing business in China. Baiguan is trusted by over 100 global institutional investors, diplomats, corporate executives, CIOs, industry specialists, and curious minds from more than 80 countries.

| A guest post by

|

It's interesting that while the first part of the analysis says that consumption is weak, at least two of the policy prescriptions (hukou reform and electricity pricing reform) have nothing to do with addressing the problem (i.e., stimulating consumption). To be sure, hukour reform and electricity pricing reform are good policies to pursue, but they are justified on other grounds (i.e., making the economy more efficient, productive) and have nothing to do with stimulating demand.

Just my take!

Thank you. I live in NZ so my comments may be irrelevant. Capitalism!!! in my understanding was at times in the USA driven by the "Robber Baron" who developed railways, steel manufacturing, automobiles and etc. So in many ways totally unregulated. I'm not saying I agree with this. But, it also unleashed creativity and at times amazing innovation. For example Edison, and Tesla, I guess I should add Elon Musk, even though I'm not describing him as a robber baron. So in a controlled economy how do we unleash this creative capacity? Respectful greetings. Richard Wheeler