Hello! In today's post, I'm sharing a summary of two fascinating articles on China's new energy and automotive industries, which I discovered on 微信公众号 (WeChat Blog), a platform akin to Substack.

Recently, there has been a widely circulated article on WeChat titled “卷王”经济学 The Economics of "King of Involution", which is about the reflections of Will Shen, a German investment and M&A professional in the automotive and new energy sectors, upon returning to his home country China. Will discusses the intense competition and the future of China's manufacturing industry in the new energy sector.

Will’s article receives over a hundred thousand views (a popular view count on social media in China). Then, another article titled 为什么卷王经济学是断头路 Why is the Economics of "King of Involution" a Dead End came out and presents a different perspective. It suggests that the price war resulting from such intense competition harms both labor and capital, and emphasizes the importance of a healthy competitive environment in the industry to ensure a reasonable profit margin for all stakeholders.

The article was written by Bob Chen, a seasoned investor at Mangrove Capital 沣源资本, a China-based venture capital fund specializing in software and globalization-themed investments.

Before discussing these articles, it is important to clarify the concept of "involution," which is the English equivalent of the Chinese buzzword "内卷" (Neijuan). In China, "involution" refers to the phenomenon of the rat race, burnout, and diminishing returns, where putting more into something only results in getting less back. Based on this concept, "卷王" (Juanwang), or "King of Involution," refers to those who are most avid or leading in the involution.

In 'The Economics of the "King of Involution",' Will argues that the pressure of 'involution' spurred rapid growth in the automotive and new energy sectors. He suggests that once COVID-related restrictions were lifted, Chinese companies, dubbed the 'kings of involution,' dominated the global market. Meanwhile, in 'Why the Economics of the "King of Involution" is a Dead End,' Bob expresses concerns about the sustainability of this model.

The following are the summaries of key ideas and highlights from the two articles.

Part 1 - The Economics of "King of Involution"

1. Living in Germany, the author worked at investment, mergers and acquisitions in automobile and new energy sectors for over twenty years, and he observed that the competition in China's energy and automobile markets is the most intense on a global scale.

For example, photovoltaic (PV) company lost a 1 gigawatt (GW) order to its rival simply because an employee forgot to hide the client company's logo when celebrating the deal on WeChat Moments one day before finalizing. The competitor's offer was just one fen (one hundredth of a yuan) lower.

For instance, an electric vehicle (EV) charging pile manufacturer, in the process of preparing to launch its next-generation products, discovered that its competitor had already rolled out 50KW DC fast charging piles, all within the same dimensions as the 7KW AC charging piles.

比如说,储能电池产能暴增,价格暴跌,部分280Ah出货价格跌至0.25。

For another instance, the price of energy storage batteries plummeted amid a surge in output, with some 280Ah battery cells priced at 0.25 yuan/Wh.

2. However, with a surge in production capacity and a subsequent slump in prices, companies within the sector are experiencing a sharp decline in profits.

我带的老德在东南某省的某企业谈判的三天内,同时在现场考察和谈判的还有印尼,中东,意大利和韩国的另外四批客户。公司海外市场销售总监在各个会议室之间跑来跑去,忙的鸡飞狗跳。 During the business trip, I spent three days helping a Germany company negotiate with a Chinese company in a Southeast China province. Joining us were representatives from Indonesia, Italy, South Korea, and a Middle East country. The director of overseas sales for the Chinese company was busy running between conference rooms during our visit. 由于这些海外客户远较国内客户慢得多的项目进度,预计形成大规模销售的时间大多在2024年下半年乃至2025年上半年。 Given that projects with these overseas customers are progressing at a much slower pace than its domestic customers, large-scale sales are expected to come by the second half of 2024 and even by the first half of 2025.

但该公司的三季报却是上市以来最烂的。 But the company just reported the worst quarterly financial results since it got listed.

国内市场销售的产品2023年价格暴跌,导致公司销售额持平的同时,利润更是大幅下跌。营收账款增加,负债增加,同时研发支出和资本支出同样大幅增加。结果就是股票今年跌了将近50%,投行金融机构纷纷看衰。As domestic sales prices slumped this year, the company suffered a sharp decline in profit while keeping sales flat. At the same time, account receivables and liabilities increased while R&D and capital expenditures grew significantly. The consequence was that its stock prices fell by almost half this year, leading to bearish forecasts from various investment banks and financial institutions.

与此类似的企业还有一大批。 A lot more Chinese firms are experiencing a similar situation.

3. Despite financial challenges, companies still invest heavily in R&D and capital expenditures. Why? In fact, this signals their navigation through a transitional phase, which is the real story unfolding for many Chinese companies during the transitional period of the Chinese economy.

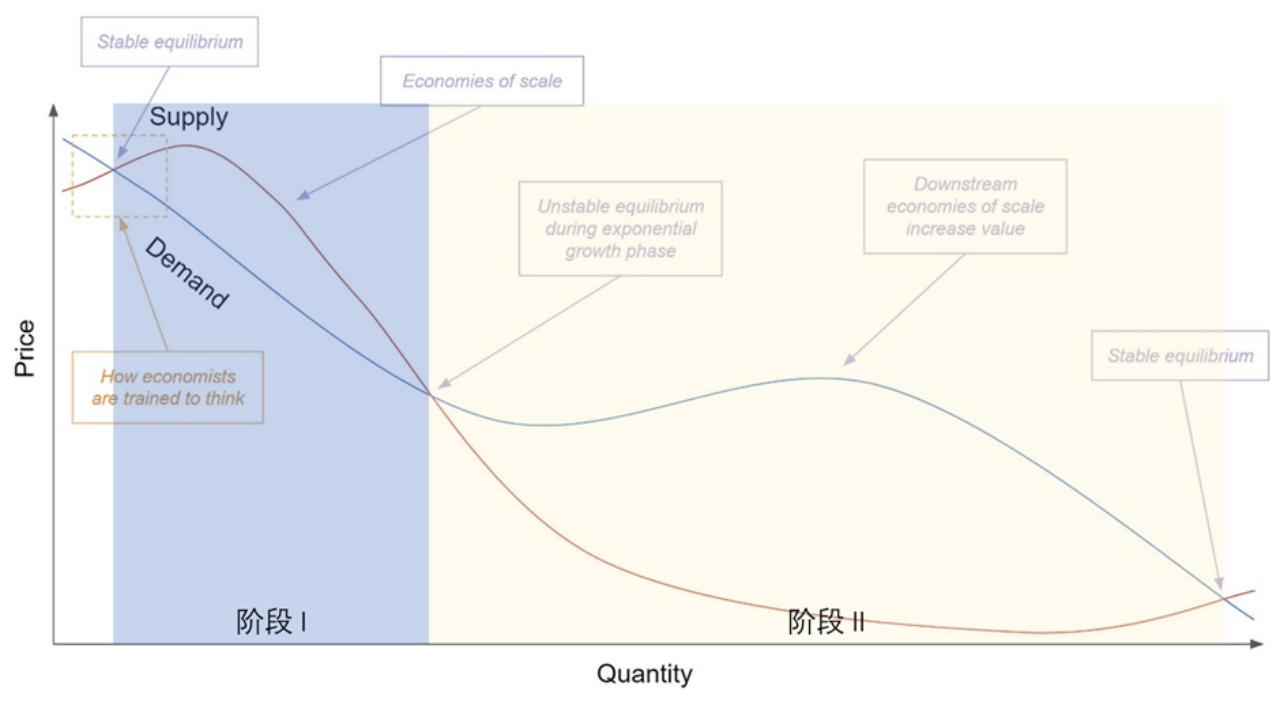

The figure below illustrates how the price and output of a new technology or product changes as supply and demand change. In a fully competitive market, a firm suffers a loss in Phase I before gaining a profit in Phase II. Most firms wish to shift from Phase I to Phase II at the fastest speed.

There are two ways to do that.Businesses can either invest heavily in production and scale up through massive capital expenditures, or invest heavily in manufacturing process R&D and increase manufacturing efficiency through technological innovation. Both will require hefty capital inputs in Phase I when a firm has difficulty selling its products and makes a meager profit, causing its income statement and balance sheet to deteriorate simultaneously.

This is the real story unfolding during the transitional period of the Chinese economy. Facing fierce competition in an era where new iterations of technology take off quickly driven by the ongoing technological revolution, numerous enterprises report weak results in their income statement, balance sheet, and even cash flow statement. Pessimism should have been widespread from a financial and investment standpoint, but businesses remain broadly optimistic, expecting the highly rewarding Phase II to come quickly as the market matures. This explains why they are still investing big in R&D and capital expenditures (more being capitalized R&D expenditures). Industrial power consumption is hitting new highs again and again only because of improving PMI data.

4. Some concern that these intensive capital expenditures will result in massive waste of resources. Such worries are unnecessary, because in knowledge intensive industries, most of the investments are directed towards R&D rather than raw materials, which means they will not be wasted once the old capacity phases out, but will contribute to developing new capacity. Also, excess capacity does not compromise the profitability of new capacity; in comparison, the latter loses out entirely in terms of cost and efficiency.

Today firms’ capital expenditures mostly go into high-tech automated production lines and high-precision equipment. And these equipments have been domestically manufactured and supplied on a large scale. High-precision equipment manufacturing is a knowledge intensive industry.For a battery formation and grading system that can cost a battery manufacturer hundreds of millions of yuan, more than half of the cost is thousands of engineers hired by the automation manufacturer or upstream equipment manufacturers. The raw materials contained therein may account for less than 30 percent. Such capital expenditures are in fact R&D inputs to the entire supply chain. In the short term, these devices may be replaced and generate potentially gaping holes in a firm’s balance sheet, but they actually represent the experience accumulated by R&D personnel and engineers and all sorts of intellectual property rights.

...

随着技术迭代和工艺提升,老旧技术和产能是毫无竞争力的。

As new iterations of technology emerge and manufacturing process improves, old technology and production capacity would completely lose their competitiveness.

For example, global new solar PV capacity is forecast to reach 402GW in 2023, bringing the total capacity to more than 800GW, and the global PV new installations are expected to reach 446GW in 2023. But in fact, about 500GW of the 800GW total capacity comes from TOPCON and HJT batteries, while the remaining mostly comes from old PERC batteries. Compared with the former, the latter is not competitive at all in terms of cost and efficiency, and is useless capacity for the real market.

5. A key condition enabling this unique "involution" was the country's stringent pandemic control measures, which led to an isolated, yet gigantic market that spawned stiff domestic competition. In this setting, the speed of evolution within China's industrial ecosystem far surpasses that of overseas counterparts. Coupled with other factors such as strong localization and marketing strategies, Chinese companies hold substantial advantages when expanding overseas.

Extremely stiff competition within an isolated, yet gigantic Chinese market prompts China’s industrial ecosystems to evolve several orders of magnitude faster than overseas markets. At the same time, due to the regional disparities in both geography and developmental levels across the country, enterprises nurtured by the Chinese market are often capable of providing products tailored to diverse ecosystems with different customer needs.

As Chinese firms enter Phase II after fast product iterations in the domestic market, overseas markets are usually still in Phase I, albeit at different levels. During this period, overseas competitors struggle to increase investment to expand the scale, while the prices customers consider to be acceptable are at high levels. So when a Chinese firm steps into an overseas market with a proper localization strategy, coupled with an excellent marketing strategy and a viable sales channel, that market will directly move to Phase II. This is how Chinese EVs grab market share overseas.

三年疫情恍如隔世,而今年是汽车和新能源领域中国企业王者归来的一年。汽车和能源是全球工业领域价值最高,产业链最长,覆盖领域最广的两个,完全可以称得上是人类工业化的皇冠。国之有幸,在于当我们基础工业和积淀基本完成的时候,恰如其时的进入了新一轮能源革命带来的全球变革之中,使我们能够将人口,体量,规模和产业集聚效应等所有因素发挥的淋漓尽致。这是未来50-100年中国工业和经济维持全球领导地位的基本保障。 So many changes have taken place in the past three years. This year has witnessed Chinese firms’ comeback in the auto and new energy sectors. Across the global industrial sector, auto and energy, which have the highest value, feature the longest industrial chain, and cover the widest fields, can be regarded as the crown jewel of industrialization. China is lucky to embark on a new round of global energy revolution just in time after the country has laid a solid industrial foundation, enabling it to take the most advantage of all factors, including population, size, scale, and industrial agglomeration effect. This will help ensure China’s industry and economy maintain a global lead in the next 50 to 100 years.

在这个无比坚实的基础之上,那些所谓的金融市场也好,汇率市场也罢,货币政策还是财政政策,真真假假的外资在我们的资本市场上出出进进的忙里忙外,对于我们而言不能说是无足轻重,只能说是毫无影响。 Based on such a solid foundation, China will be immune to fluctuations in financial and foreign exchange markets, monetary and fiscal policies, and flow of foreign capital into and out of the country, whether real or not.

6. It's worth noting that China's manufacturing industry shows a promising upward trend, as evidenced by the substantial increase in energy consumption — a vital indicator of the nation's industrial prowess. As a key metric for China's manufacturing-driven economy, its energy consumption is on the rise.

China’s energy consumption is growing wildly, with a whopping increase of 8.4 percent in October, for example. Industrial energy consumption rose for five consecutive years, even during 2020 and 2022 when the toughest pandemic controls were in place.

...

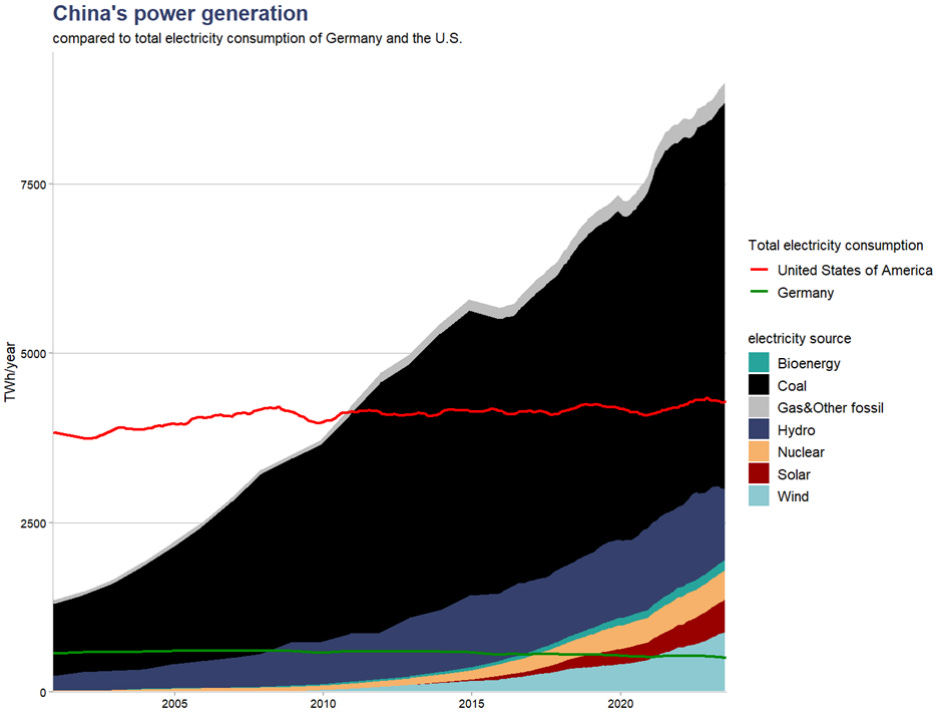

最后附一张在推特看见的2000年至今中国发电量增长的图。

The figure below shows the growth of China’s power generation since 2000 (The figure was posted on U.S. social platform X, formerly known as Twitter).

其中红线为美国的全国能源消耗,绿线为德国的全国能源消耗。

The red line represents total electricity consumption of the U.S., while the green line indicates total electricity consumption of Germany.

Looking back, China’s power generation didn’t surpass that of the U.S. until 2010. But today, China’s power generation is double the electricity consumption of the U.S. In other words, China’s newly-added electricity demand since 2010 equals the total electricity consumption of the U.S. Of the new power generation capacity, more than 60 percent has ended up in supporting industrial activities.

而从人均来看:作为世界人口第一(今天已经是第二)大国,我国的人均用电量去年超过了德国。

At per capita levels, the per capita electricity consumption in China with the world’s largest (now the second-largest) population surpassed that of Germany last year.

Subscribe GRR newsletter for free to get a glimpse into the priorities of both the leadership and the general public in China.

Part 2Why is the Economics of "King of Involution" a Dead End?

[Note: Bob Chen, the author of the second article, possesses significant expertise in investing in Chinese enterprises that are expanding globally, often referred to as 'Go Global 出海' companies.]

1. Involution within China's new energy sector causes damage to both workers and the running of companies, and a healthy competitive environment within the industry is imperative in ensuring a reasonable profit margin for all stakeholders.

The Economics of "King of Involution" presents two dividends brought by involution. First, China's new energy sector has cultivated a large number of engineers and a labor dividend. Second, the sector holds substantial competitive advantages that it can sweep the international market upon accessing it.

Regarding the first point, I totally agree, but I don't think it's something the labor should be happy about. The flip side of the dividend is the exploitation of surplus value. Businesses that use labor exploitation to obtain a global pricing advantage will not increase wages for their employees even if their market share grows internationally. Not to add that, in this day and age, involution prevents even entrepreneurs from making money. Therefore, even though there is a labor dividend, labor itself shouldn't take pride in it; instead, working abroad will allow them to benefit from the pay gap dividend.

Second, in my experience as an international investor, Chinese businesses are increasingly undercutting one another by offering low costs. They performed poorly, though, when it came to spending money on post-sale support channels, brand culture, and—above all—making money.

China will be an enormous economic entity, but businesses inside the country cannot profit due to overextending all available labor.Furthermore, as The Economics of "King of Involution" explains, these businesses must continually invest in building and dismantling production lines for ongoing technological innovation, occasionally scrapping before depreciation. In the end, neither capital nor labor components profit financially.

Only when Chinese businesses are willing to make profits for themselves, abandoning the goal of involution in favor of more orderly competition, will national income and corporate profits truly rise.

2. The steady increase of China's per capita income results from investing resources, comprehending production line construction, learning new technologies while working with OEMs, and having entrepreneurs find products that fit the market. Price wars, one-dimensional investments, or repetitive investments related to the involution are not the cause.

Some claim that the success of PDD's overseas expansion (Temu) is proof positive of involution. This is untrue. Rather than just copying Alibaba's business model, PDD, even at home, sought to set itself apart by reaching out to a customer base with less purchasing power. Through the integration of multiple upstream factories and quality control capabilities, they exported China's e-commerce experience abroad, resulting in a transnational "Chinese-style" transformation for different stages of fulfillment. They looked for regional American businesses that are seldom seen by outsiders, even in the most conservative and traditional field of last-mile delivery in the United States. They investigated the competitor's location advantages and cost structure in great detail, trying to incorporate them into their own fulfillment network.

In the global market, few predecessors have adopted such practices. Even Shein has not fully globalized China's supply chain experience, despite its widespread presence.

3. The main reason Chinese companies are willing to compromise profits is primarily rooted in the government's encouragement of investment and export-oriented mechanisms, leading companies to pursue marginal cost competition, neglect fixed costs, and engage in global markets through low-price competition to meet global consumer demands.

Investment creates GDP, so local governments encourage investment by offering preferential measures such as land and tax concessions to generate immediate GDP.China is not lacking in capital; rather, it lacks innovation capability. For entrepreneurs lacking in differentiation and strategic thinking, the best approach is to follow pioneers, adhere to established technological paths, save on innovation costs, and avoid innovation risks.

因此,即使你做到了行业老大,你也不一定能够赚钱,因为中小玩家会以边际成本来市场上跟你竞争。

Therefore, even if you become the industry pioneer, there is no guarantee that you will make a profit, as smaller players may compete with you in the market based on marginal costs.

According to market economy theory, at the peak of competition, the price of every good equals its marginal cost of production. This is extremely uncommon, though, as marginal costs can be variable or even close to zero, particularly in the case of increased industrial product production where assembly line costs are almost zero.

Once everyone exerts full effort, producing based on marginal costs and completely overlooking the previously invested factory and fixed asset costs to compete on price, this becomes extremely concerning. However, this is a situation encountered in many industries in China. Even when expanding overseas, companies may employ this approach to seize market share.

最后就变成了全球消费者们的狂欢,尤其是可以用手头的美元来换取我们制造能力的国家。

In the end, it turns into a global celebration for consumers, especially for countries that can use dollars to acquire our manufacturing capabilities.

4. In addition to overseas consumers, who enjoy the dividend of involution include: few entrepreneurs, especially if they go public and profit from the appreciation of equity; players controlling upstream raw materials, benefiting from the highly monopolistic nature of the industry.

What are your thoughts on these two differing perspectives? We welcome and encourage your comments!

Thanks for the interesting article. “Involution” is a difficult concept to understand. I am not sure the English meaning really corresponds to the Chinese meaning. The English dictionary defines “involution” as a mathematical operator that when applied twice in succession, returns the original state. It is also a biological idea, being some organ that returns to its original state.

The Chinese concept reminds me of the Red Queen in Alice’s Wonderland, who runs hard but still remains in the same position. So the Chinese Involution seems to mean “running hard but getting nowhere”, or “putting in a great deal of effort but getting nothing in return”.

I suppose “Involution” is the best translation of 内卷: not achieving any progress despite exerting oneself.

The picture drawn by the second author reminds one of the U.S. in the middle of the nineteenth century. Competition was ruinous, approaching the textbook model of perfect competition. This phase had to end. It ended with the formation of monopolies, known at the time as "trusts" - the Steel Trust, the Sugar Trust, etc.

How will the "involution" phase end in China? One difference is that the U.S. was not the main player in the scramble for imperial domains. Britain, France, and Germany fought that scramble of exporting capita to acquire external markets and secure sources of raw materials. China is already deeply enmeshed in the similar scramble today. It led to world war then.

Thanks for the interesting article. “Involution” is a difficult concept to understand. I am not sure the English meaning really corresponds to the Chinese meaning. The English dictionary defines “involution” as a mathematical operator that when applied twice in succession, returns the original state. It is also a biological idea, being some organ that returns to its original state.

The Chinese concept reminds me of the Red Queen in Alice’s Wonderland, who runs hard but still remains in the same position. So the Chinese Involution seems to mean “running hard but getting nowhere”, or “putting in a great deal of effort but getting nothing in return”.

I suppose “Involution” is the best translation of 内卷: not achieving any progress despite exerting oneself.

The picture drawn by the second author reminds one of the U.S. in the middle of the nineteenth century. Competition was ruinous, approaching the textbook model of perfect competition. This phase had to end. It ended with the formation of monopolies, known at the time as "trusts" - the Steel Trust, the Sugar Trust, etc.

How will the "involution" phase end in China? One difference is that the U.S. was not the main player in the scramble for imperial domains. Britain, France, and Germany fought that scramble of exporting capita to acquire external markets and secure sources of raw materials. China is already deeply enmeshed in the similar scramble today. It led to world war then.