What's Huawei's master plan for electric vehicles?

"Not making cars might be harder than making cars for Huawei."

On August 8, the much anticipated electric vehicle brand Avita 11, which Huawei has been deeply involved with, was officially launched.

As we showed in a previous post analyzing Huawei's 2021 annual report, smart electric vehicle has become a centerpiece of this technology giant's strategy.

The following article posted by YuanChuan, a research company, illustrated the very delicate line that Huawei treaded between being a "Tier-0.5" supplier and a full-fledged automaker. Whatever it will ultimately become, Huawei is destined to join the ranks of Tesla, BYD and CATL to stand at center stage in the global EV industry.

The original title of the article is 华为不造车,也许比造车更难 Not making cars might be harder than making cars for Huawei.

At the Chongqing International Auto Exhibition that just ended not long ago, Changan Automobile's 长安汽车 sub-brand Avita became a show stopper. [The city of Chongqing is a municipality in southwest China]

Even though not a car has yet been sold, Avita was already valued at 200 billion yuan (about 29.6 billion US dollars) by China Securities International 中信建投, which was even higher than the valuation of its parent company Changan Automobile. Moreover, at the press conference, Huaiwei's current rotating chairman Xu Zhijun 徐直军, CATL宁德时代's chairman Zeng Yuqun 曾毓群, and Changan Automobile's chairman Zhu Huarong all joined forces to promote Avita. The CEO of Avita, Tan Benhong, was also on stage, echoing others.

Almost no other new brand has enjoyed such an extravaganza.

Avita was officially founded in November last year. With Changan Automobile and CATL being its shareholders, and Huawei's deep involvement in the R&D, the company presented its first prototype car -- Avita 11, in just eight months.

It is safe to say that this car combines Changan Automobile's anxiety about transformation, CATL's ambition for the value chain [expansion], and more importantly, Huawei's desire to verify the success of the "supplier model".

Huawei has stated on several occasions that it "does not build cars, but focuses on ICT technology to help car companies build good cars". But it is said that Huawei has sent a team of 1,000 people to Chongqing to assist the development of Avita 11.

Considering SAIC Motor's chairman Chen Hong 陈虹's "soul theory" comment not long ago, and Huawei's former cooperation with Seres SF5 and ARCFOX 极狐 can hardly be considered as successful, Avita 11's performance in the market might influence whether Huawei's "supplier model" can be accepted by most auto OEMs. [red_wallstreet: SAIC Motor's Chen Hong, when asked about whether SAIC will cooperate with third-party providers like Huawei in autonomous driving, he responded: "In such case, they will become the soul, SAIC will only be a body. This is unacceptable for SAIC. We must control the soul."]

This is a technical problem, an industry problem, and also a business problem.

01 TIER 0.5

To understand Huawei's "supplier model", it is necessary to review what has changed in the supply chain when traditional gasoline cars evolved into smart electric vehicles.

The structure of the traditional automotive industry is similar to a pyramid, where the OEMs are at the top. They outsource components to manufacturers on lower tiers. For example, the door system is outsourced to Tier 1 suppliers, and then the Tier 1 suppliers outsource the window system to Tier 2 manufacturers. Next, Tier 2 manufacturers further outsource the window regulators of the window system to Tier 3 suppliers. So on and so forth, a stable supply chain is thus formed.

The supply chain structure of the traditional automotive industry

But the other side of stability is isolation. For one thing, Borsch, ZF and other large Tier-1 suppliers were established in the late 19th century, and they have constructed extremely high barriers of patents after taking up 70 percent to 80 percent of the car components manufacturing. For another, in the 1990s, OEMs split their internal supply chains, creating a number of Tier 1 companies like Delphi and Visteon. Those companies are closely tied with OEMs.

Traditional OEMs and Tier 1 manufacturers built a high wall together, rejecting others entering the automobile supply chain. Theoretically speaking, all suppliers below Tier 1 were determined by OEMs and Tier 1 manufacturers.

Therefore, the advent of electric vehicles is rather a complete do-over of the supply chain than a switch in energy sources.

For instance, the 48V battery used in traditional vehicles wasn't worth much. But right now, the battery has turned into a core component, accounting for 40 percent of the total cost of a vehicle. The core of the drive system has changed from engine and transmission into electric drive and electric control. A large screen that integrates almost all the functions is now installed in the cabin, which means software and operating systems have become more important than ever.

The revolution of end products also affected the upper stream of the industry chain, bringing about two huge changes.

The first change is the emergence of new supplier giants, such as LG and CATL in the field of power batteries. The second one is the trend of industry chain integration. For example, BYD launched an eight-in-one electric drive system on its e3.0 platform, and Tesla integrated into three domain controllers functions that would've been defined by hundreds of ECUs (Electronic Control Unit) in traditional cars.

The speed of industrial change far exceeds traditional suppliers' pace of adaptation. On the other hand, Tesla has been improving its integration capabilities all along. Hence, in terms of the hard power and development capability of car intelligence and electrification, Tesla is already miles ahead of many companies that rely on traditional suppliers.

But not all OEMs have such superior R&D capabilities as Tesla does, and there are always OEMs who need someone to integrate intelligent and electrified component modules from different Tier 1 suppliers, and provide them with a turnkey solution.

In a nutshell, the once closed automotive supply chain starts to teem with new opportunities, and companies offering integration plans are beginning to benefit from this wave.

Thus, a new role of Tier 0.5 manufacturers, positioned between Tier 1 manufacturers and the OEMs, was born. This is where Huawei is located. The most critical of Huawei's self-definitions is being the "smart car incremental parts supplier". As Xu Zhijun said, "We will not do what the traditional automotive supply chain has."

But his words also implicate that "we will do whatever the traditional automotive supply chain does not do."

02 RETREAT TO ADVANCE

Huawei indeed chose this strategy.

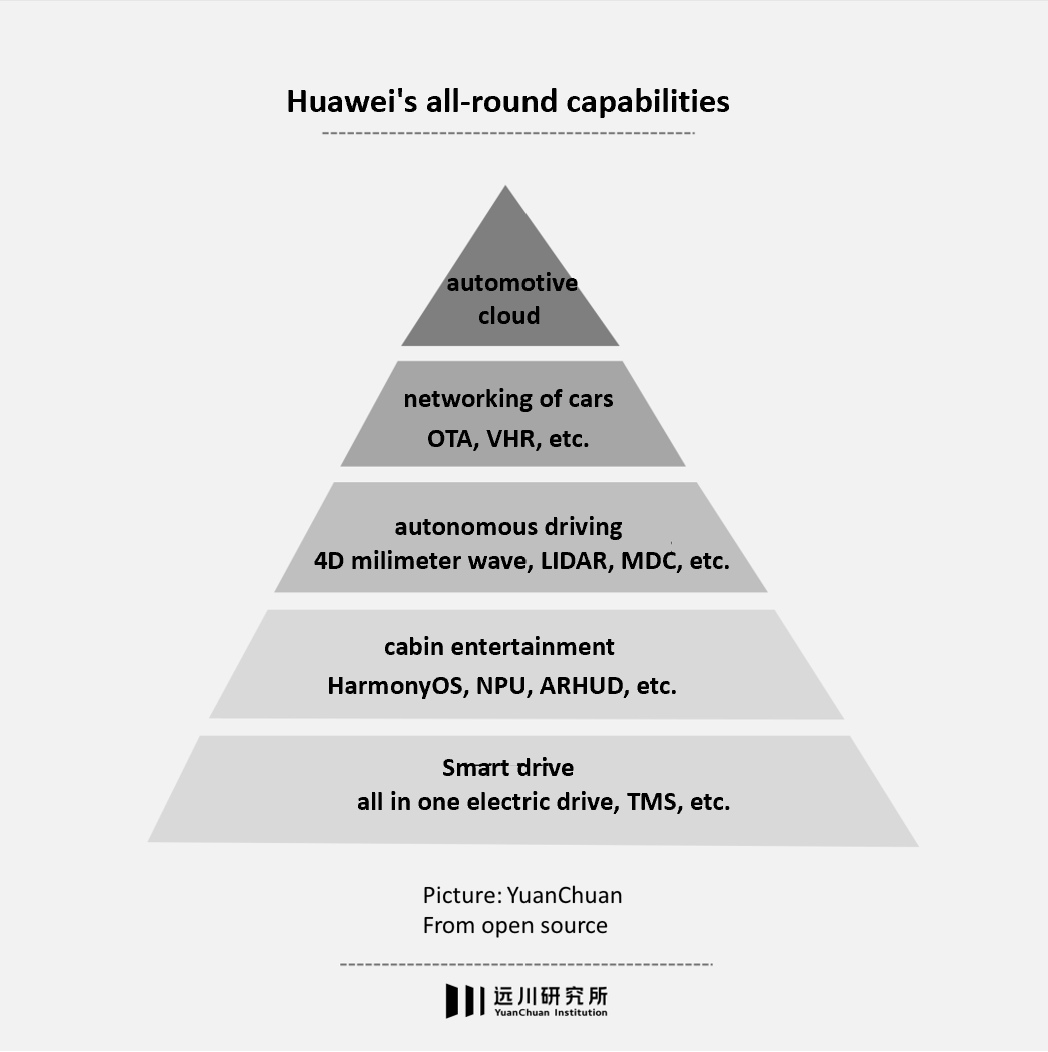

At the Shanghai Auto Show held in April 2019, Huawei made its debut as a supplier, bringing a family package for smart electric vehicles: the CC Solution (Computer and Communication), plus five major smart electrification platforms, including automotive cloud, the networking of cars, autonomous driving, electric drive, and cabin entertainment.

In short, except for the battery, chassis and body of cars, Huawei has done everything.

Behind Huawei's all-around capabilities are technologies it developed in various businesses.

Take smart cabin, where customers interact the most, as an example. In AITO M5 and AITO M7, the most notable is the operating system with a 2K screen, which greatly outperformed the products of other carmakers. The operating system has hardware like the display panel, cabin chips, and power modules, as well as Huawei's HarmonyOS system including maps, the smart speaker, and other software.

This is actually the core formula for Huawei to become a Tier 0.5 manufacturer: integrating technologies in other fields and that of Tier 1 manufacturers, connecting them together, and eventually forming its own unique platform solutions.

It is this integration capability that scares the OEMs. Because the largest technology hub in the traditional industry chain is the OEMs. In other words, building a car is not difficult for Huawei.

This is where the public is most puzzled by Huawei. Since it has the ability to become a Tier 0.5 manufacturer, why not simply build a car?

There is no official answer from Huawei to this question, but the reason is not difficult to guess: the competition of OEMs in China is extremely intense. And today there are more than 130 domestic brands fighting against each other, far more than markets in Europe or the United States. When Xu Zhijun visited the major domestic car companies, he received the same reply: China's auto market does not need a new car brand.

On the contrary, the trend of intelligent development and electrification, plus the trend of providing domestic alternatives for the supply chain, are something China's suppliers have waited for a long time.

The first trend almost erased the century-long tech accumulation of traditional suppliers in the gasoline car field. For example, NGK, a company that has produced spark plugs for more than 80 years announced it will abandon internal combustion engine technology for power batteries.

The second creates lots of vacancies in the domestic supply chain. China's automotive supply chain has never had such an integrated supplier as Bosch in its history. But nowadays, whether it is 均胜电子 Joysun Electronics, which is in a frenzy of acquisitions in the field of automotive electronics, or Huawei, which is trying to provide a whole set of intelligent solutions for car companies, is fighting over these vacancies.

Moreover, Huawei is more of a company facing enterprise customers. Although most of its popularity comes from its cell phone business, from its earliest communication business and carrier services, to cloud services and energy business, Huawei's edge is in business for enterprises.

In the automotive industry, suppliers can focus on technology R&D and supporting OEMs, but OEMs have to deal with extensive and complex problems of the supply chain, production process and even users. Therefore, the former is obviously more matching with Huawei's R&D capabilities.

According to Yu Chengdong 余承东 ( CEO of the Consumer business group at Huawei Technologies ), Huawei's investment in the automotive business reaches more than one billion US dollars per year, and the number of people directly involved and indirectly involved in R&D is up to tens of thousands of people. The autonomous driving system for ARCFOX, Huawei's first such attempt at a high completion level, was the direct result of such a high level of investment.

At least in China, there are not many mass-produced autonomous vehicles that can achieve this level of success, and this is the core of Huawei becoming a Tier 0.5 manufacturer. And whether it can gain a foothold in Tier 0.5 depends on two things.

(1) Maintain the generation gap advantages. Just like in the cell phone industry, Qualcomm's excess profit lies in its products' performance advantage over other SoC design companies. Once other competitors such as MediaTek catch up with Qualcomm, then a fierce price war is very likely to happen.

But this doesn't seem to be too difficult for Huawei, considering it is known for its R&D capability.

(2) do not touch customers' business: Qualcomm and MediaTek only design chips, and never make cell phones, which is often the basis for mutual trust between upstream enterprises and downstream enterprises in the industry chain. However, it is the biggest uncertainty hovering over Huawei.

Will Huawei be willing to just become Qualcomm? This is a question that all OEMs have to think about.

03 DEFINE BOUNDARY

The automotive industry's attitude toward Huawei has been ambiguous so far, and the most well-known event is SAIC Motor Chairman Chen Hong's "soul theory".

When we spoke with a colleague at the research institute of FAW 一汽 in 2021, he was also vague about Huawei: "We respect Huawei's technical strength, but the cooperation for the whole plan needs to be considered carefully."

Never getting their hands on the downstream business easily is a law obeyed by suppliers and OEMs. Arm only does IP licensing, Qualcomm only does chip design; BOE京东方 doesn't make TV sets, TSMC 台积电 doesn't do chip design. Although Google once made its own cell phone, it wasn't serious about sales. Their phone was like socializing and was only seen as a sample for the Android system.

For IDMs (Integrated device manufacturers) involved both in upstream manufacturing and downstream manufacturing, the chain often tends to stay within its own system. For example, Intel made chips for its own chip services. It only started making chips for others in recent years. Before AMD sold GlobalFoundries, it also made its own chips.

Samsung may be one of the few counter-examples —— besides producing parts for others, it has a bunch of chip businesses, plus making end products such as cell phones and TVs. The result is that Apple, its major customer, is filing a lawsuit against Samsung while secretly supporting TSMC. It is no wonder that Shi Zhengrong施正荣 (a Chinese-Australian businessman and philanthropist) said: Samsung is the enemy of the world.

Huawei's approach in various industries is more or less like that of Samsung. First, it focuses on making a breakthrough in the part with the highest added value, then it penetrates downward slowly to obtain the profits of the entire industry chain. Huawei once said " We would never make cell phones". But when the wave of smart phones came, many domestic phone brands were hit hard by Huawei.

Therefore, the "soul theory" is not out of thin air. For Huawei, the way to reassure car manufacturers is to establish their own supplier boundaries as soon as possible.

In January 2019, Huawei quietly signed contracts with Sokon 小康, BAIC Motor 北汽, and Changan Automobile, to validate Huawei Smart Choice 华为智选 and Huawei Inside.

Huawei's cooperation with Sokon and BAIC Motor was very successful, and the two hottest topics at the 2021 Shanghai Auto Show are the Seres SF5 and the ARCFOX autonomous driving.

The former is a product built in the United States by Zhang Zhengping 张正萍, son of Sokon's chairman. From the driving system to the front-wheel-drive, and even the car's air conditioning are all provided by Huawei, plus Yu Chengdong advertised the car himself, Huawei is heavily involved. The latter is the first model equipped with Huawei Inside, equipped with Huawei's self-driving program. The demonstration video went viral on the Internet.

However, from the follow-up effect, the two collaborations are hardly successful. Seres SF5 only sold 8,169 cars around the world last year. It got 6,000 orders after a week on the market, showing how weak the sales were. To free up production capacity for the new car AITO M5, it also suspended production for other products.

In addition, Huawei was at an extremely strong position in the cooperation, and Sokon Automobile shared all kinds of information with Huawei, including the R&D of Seres, the purchases, production data, and even the timetable of assembly line workers. Huawei was responsible for the design and technology of the Seres M5 from start to finish, so the claim that Sokon was working for Huawei is not groundless.

ARCFOX experienced repeated delays of the Alpha S HI version. Some investors blamed ACRFOX for the delays, but ARCFOX felt wronged. In a report by Autobit citing Cls.cn, officials from BAIC BluePark New Energy 北汽蓝谷 said: "Huawei is a dominating supplier. We have not been involved in the software. Now the operating system of HarmonyOS is not available, we are also waiting."

In these two collaborations, instead of highlighting Huawei's Tier 0.5 positioning, the partners' cars were seen as a "Huawei brand".

It wasn't until the advent of Avita, the product of cooperation with Changan Automobile, that things changed.

For one thing, Changan Automobile has a strong brand, which reduced some of the "Huawei brand" tint. For another, in terms of R&D capabilities, Changan's "Beidou Tianshu" project has a software R&D team with a thousand members, which means it is in an equal position with Huawei.

With Changan's endorsement, Huawei's positioning of a supplier is much clearer than before. However, the sales of Avita may determine where the road of Tier 0.5 leads for Huawei.

04 THE EPILOGUE

Huawei is not the only company trying to become a Tier 0.5. At Apple's Worldwide Developers Conference on June 7, Apple made a rare report about its Carplay performance. About 98 percent of cars in the U.S. now support Carplay and 79 percent of U.S. consumers say that they would only buy a car that supports Carplay.

Before Huawei became an auto brand, competitors across the ocean had already taken the lead in planting a flag in the minds of consumers.

Along with the frequent iterations of Carplay, Apple has gone from the "car navigation provider", step by step, Apple is now able to deeply integrate Carplay with the hardware of the vehicle. It even acquires vehicle data directly from the operating system, which is not too different from the Harmony OS that is already on board.

Maybe in the next five years, these two companies will fight against each other in the automotive industry, just as they once did in the smartphone industry.

To help make GRR sustainable, please consider buy me a coffee or pay me via Paypal. Thank you for your support!